The car insurance bill you forgot was annual. The laptop that died after four years of warnings. The wedding you’ve known about since February. None of these are emergencies — they were completely predictable. But because they weren’t in the monthly budget, they hit like emergencies anyway.

That’s what a sinking fund solves. It’s the single most underused personal finance tool for people who already have a budget but still find themselves blindsided by large planned expenses every few months.

This guide covers exactly what a sinking fund is, how it differs from an emergency fund and a savings account, 20 categories worth having, a step-by-step setup process, how much to put in each one, and where to keep them — including a specific breakdown for expats managing irregular large expenses in the UAE and Gulf region.

Why Your Budget Keeps Getting Ambushed

Most people budget for the same expenses every month — rent, groceries, utilities, subscriptions. The budget looks reasonable on paper. Then October arrives and car insurance is due. December brings flights home, holiday gifts, and a year-end dental appointment. February brings a renewal, a maintenance bill, and a birthday.

These aren’t surprises. They happen every year, often in the same months. The problem is that a monthly budget only protects against monthly expenses. It leaves annual and irregular expenses completely unaccounted for until the month they’re due.

This strategy fixes the problem by breaking annual and irregular expenses into small monthly contributions — so when the bill arrives, the money is already there.

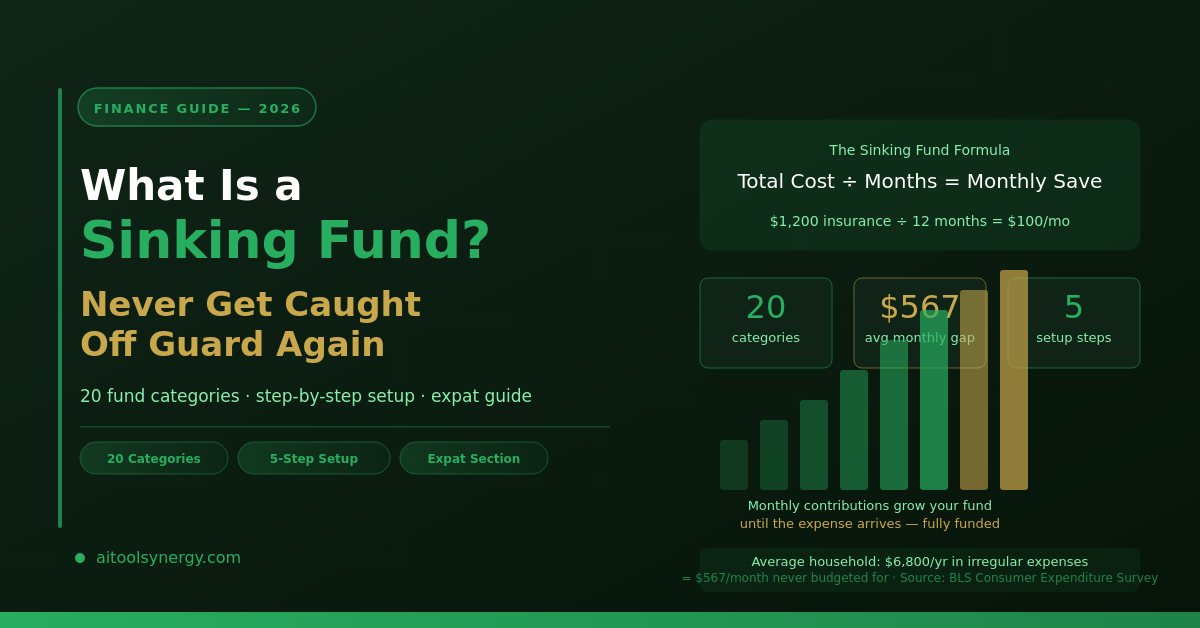

What Is a Sinking Fund — The Simple Definition

A sinking fund is money you set aside each month for a specific future expense you know is coming. You name the fund, calculate how much you’ll need and when, divide by the number of months until then, and save that amount monthly.

The sinking fund formula: Total cost ÷ Months until needed = Monthly sinking fund contribution

Example: Annual car insurance of $1,200 due in December → $1,200 ÷ 12 = $100/month into your car insurance sinking fund.

When the expense arrives, you spend from that fund — not from your emergency fund, not from your monthly budget, and not on credit. The expense was already paid for in advance, $100 at a time.

The term “sinking fund” comes from corporate finance, where companies set aside money monthly to retire debt at maturity. The personal finance version works the same way: you’re pre-funding a known future obligation rather than scrambling to cover it when it lands.

Sinking Fund vs Emergency Fund — Not the Same Thing

The most common confusion around sinking funds is conflating them with emergency funds. They serve completely different purposes and should be kept completely separate.

| Factor | Sinking Fund | Emergency Fund |

|---|---|---|

| Purpose | Planned, predictable expenses | Unexpected, unplanned crises |

| Examples | Car insurance, holiday gifts, flights | Job loss, medical emergency, major accident |

| Do you know it’s coming? | Yes — that’s the whole point | No — that’s why it exists |

| Number of them | As many as you need (5–15 common) | Just one |

| Target amount | Exactly what the expense costs | 3–6 months of living expenses |

| When you use it | When the planned expense arrives | When something unexpected hits |

| Replenishment | Restart monthly contributions after use | Top back up after any withdrawal |

Using your emergency fund for a car service you knew was coming is like using a fire extinguisher to water your plants. It works, but now the extinguisher isn’t there for an actual fire.

Sinking Fund vs Savings Account — Key Differences

A savings account holds money with no specific purpose attached. A sinking fund holds money earmarked for a specific named expense. The distinction sounds minor but changes how you think about and protect the money.

When everything sits in one big savings account, the $1,200 for car insurance looks the same as the $800 for a flight home and the $400 for Christmas gifts. When the car insurance comes due, you withdraw $1,200 and the account drops — but now you can’t easily tell whether you’ve dipped into the flight money or the gift money.

Named sinking funds prevent this bleed. Each fund has a name, a target, and a running balance. You know exactly what every pound or dollar in your savings is for. This clarity also makes you far less likely to spend the money impulsively, because you can see what it’s protecting.

20 Sinking Fund Categories — What to Save For and How Much

Here are the most common and valuable sinking fund categories, with monthly contribution estimates based on typical annual costs. Adjust every figure to your actual situation — these are starting points, not prescriptions.

Essential Sinking Funds (Start These First)

🚗 Car Insurance & Registration

Annual cost: $800–$2,400 depending on coverage and location. Monthly contribution: $67–$200. This is the classic sinking fund starter — annual, predictable, and budget-wrecking if not prepared for.

🏠 Home / Renter’s Insurance

Annual cost: $150–$900 for renter’s; $800–$2,400 for homeowner’s. Monthly contribution: $13–$200. Often billed annually or semi-annually.

🔧 Car Maintenance & Repairs

Annual cost: $500–$1,500 for a reliable vehicle. Monthly contribution: $42–$125. Tyre replacements, brake jobs, and service intervals are predictable in pattern even if not exact timing.

🏥 Medical & Dental Out-of-Pocket

Annual cost: $500–$2,000 depending on coverage. Monthly contribution: $42–$167. Annual check-ups, glasses, dental cleanings — these happen every year without fail.

🎁 Holiday Gifts & Celebrations

Annual cost: $300–$1,500. Monthly contribution: $25–$125. December is not a surprise. Setting aside money from January prevents the January credit card hangover.

Lifestyle Sinking Funds

✈️ Annual Flights Home

Annual cost: $500–$3,000+ depending on destination. For expats in the UAE, Saudi Arabia and Gulf region, the annual or bi-annual home visit is one of the largest single predictable expenses. Monthly contribution: $42–$250.

🏖️ Vacation Fund

Annual cost: $1,000–$5,000+. Monthly contribution: $83–$417. Separating a vacation sinking fund from flights-home prevents one from cannibalising the other.

💻 Technology Replacement

Annual contribution: $20–$100/month. Laptops last 3–5 years. Smartphones last 2–3 years. Saving $50/month for 3 years creates a $1,800 replacement fund — enough for a quality laptop without the shock.

👗 Clothing & Shoes

Annual cost: $600–$1,800. Monthly contribution: $50–$150. Often impulse-spent throughout the year. A sinking fund gives you intentional clothing budget without the guilt.

📚 Education & Professional Development

Annual cost: $200–$2,000+. Monthly contribution: $17–$167. Online courses, certifications, conference tickets, and books all fall here.

Home & Property Sinking Funds

🛠️ Home Maintenance & Repairs

Annual target: 1% of your home’s value. On a $300,000 home that’s $3,000/year or $250/month. HVAC servicing, plumbing, appliance repairs — the 1% rule is the industry standard recommendation.

🪑 Furniture & Home Appliances

Monthly contribution: $30–$100. Appliances don’t last forever. Saving $50/month gives you a $600/year buffer for a replacement washing machine or refrigerator without panic.

Family & Life Event Sinking Funds

🎂 Birthdays & Anniversaries

Annual cost: $200–$800. Monthly contribution: $17–$67. You know exactly whose birthdays are coming and approximately what you want to spend. This category should always have a dedicated fund.

💒 Weddings (Attending)

Annual cost: $150–$1,000+ depending on how many you attend. Gift, outfit, travel, and accommodation can add up to $300–$500 per wedding easily.

🐾 Pet Care

Annual cost: $500–$3,000. Vet visits, vaccinations, grooming, unexpected illness. Monthly contribution: $42–$250. Pet emergencies hit harder without a dedicated fund.

Financial & Admin Sinking Funds

🔄 Annual Subscriptions

Annual cost: $200–$800. Monthly contribution: $17–$67. Software, streaming services, membership fees billed annually — Spotify, Adobe, Amazon Prime, professional memberships.

📄 Taxes (Self-Employed)

Set aside 25–30% of every invoice payment into a tax sinking fund. This is the most critical sinking fund for freelancers and self-employed individuals — and the most commonly missed.

🏠 Housing Down Payment

Long-term sinking fund. Target: 10–20% of property value. Monthly contribution: $300–$1,500+. Treat it like a fixed expense and automate the transfer on payday.

🆘 Deductible Fund

Target: Your highest insurance deductible. If your car insurance deductible is $1,000, having $1,000 in a deductible fund means you can use insurance without a financial crisis.

🎓 Children’s Education

Long-term sinking fund. Start as early as possible. Even $100/month from a child’s birth creates $21,600 by age 18 before any investment growth.

How to Set Up Your First Sinking Fund in 5 Steps

List every irregular expense you had in the past 12 months

Go through your bank statements from the last year and flag every non-monthly expense. Include insurance bills, car services, flights, gifts, subscriptions, medical visits, and anything else that wasn’t a regular monthly payment. This becomes your starting list.

Estimate the annual cost and target date for each

For each expense on your list, note how much it cost and when it’s typically due. If it was $1,200 and it arrives every November, you now have a target: $1,200 needed by November. Divide by the months remaining to calculate your monthly contribution.

Prioritise — start with 2 to 3 funds only

Trying to fund 15 categories at once is overwhelming and often leads to abandoning all of them. Start with your two or three most urgent or expensive categories — usually car-related expenses, insurance, and the next upcoming large expense. Add more funds as contributions become automatic.

Open a dedicated account (or use sub-accounts)

Most online banks allow you to open multiple savings accounts and name each one. Open a “Car Insurance” account, a “Holiday Gifts” account, and a “Flights Home” account. Seeing named buckets with running balances is far more motivating — and protective — than one combined savings total.

Automate the transfer on payday

Set up an automatic transfer the same day your salary lands. If your car insurance sinking fund needs $100/month, schedule a $100 transfer to that account on payday without any manual action. Money that never sits in your current account doesn’t get spent accidentally.

How Much Should You Put in Each Sinking Fund?

The calculation is straightforward, but most guides skip the actual numbers. Here’s a worked example using a $5,000/month take-home salary to show what a realistic sinking fund allocation looks like.

| Sinking Fund | Annual Cost | Monthly Contribution | % of Take-Home |

|---|---|---|---|

| Car insurance | $1,200 | $100 | 2.0% |

| Car maintenance | $800 | $67 | 1.3% |

| Home/renter’s insurance | $600 | $50 | 1.0% |

| Medical / dental | $600 | $50 | 1.0% |

| Holiday gifts | $600 | $50 | 1.0% |

| Annual flights home | $1,800 | $150 | 3.0% |

| Technology replacement | $600 | $50 | 1.0% |

| Annual subscriptions | $300 | $25 | 0.5% |

| Total | $6,500 | $542/month | 10.8% |

In this example, setting aside 10.8% of take-home salary into sinking funds covers $6,500 of annual irregular expenses — money that would otherwise ambush the monthly budget eight times a year.

To calculate exactly how much each contribution represents of your hourly or per-paycheck rate, our free Salary to Hourly Calculator converts your monthly or annual salary into an hourly rate — useful for understanding the real cost of each sinking fund in working hours.

Where to Keep Your Sinking Funds

The best account for a sinking fund is accessible within a few days but not instantly linked to your spending debit card. You want friction — enough that you won’t dip into it impulsively, but not so much that accessing it when you need it becomes a problem.

| Account Type | Accessibility | Earns Interest | Good for Sinking Funds? |

|---|---|---|---|

| Current / checking account | Instant | None / minimal | ❌ Too easy to spend |

| High-yield savings account | 2–3 business days | Yes (4–5% APY) | ✅ Best option |

| Standard savings account | 1–2 business days | Minimal | ✅ Good option |

| Money market account | Same day to 2 days | Yes (competitive) | ✅ Good option |

| Stocks / investment account | 3–5 business days + risk | Variable (loss possible) | ❌ Too risky for short-term |

| Fixed-term deposit / CD | Locked until maturity | Yes (higher rate) | ⚠️ Only for long-term funds |

High-yield savings accounts are the optimal home for most sinking funds. According to the FDIC, deposits up to $250,000 in insured US banks are protected — meaning your money is safe even if the bank fails. Look for accounts with no monthly fees, no minimum balance requirements, and the ability to open multiple sub-accounts with custom names.

How Sinking Funds Work With Different Budgeting Methods

Sinking funds aren’t a standalone budgeting method — they layer on top of whatever budgeting system you already use. Here’s exactly how they fit into the most common approaches.

Sinking Funds + Zero-Based Budgeting

In zero-based budgeting, every dollar of income is assigned a job before the month begins. Sinking fund contributions are budgeted as monthly expenses — just like rent or groceries. Your sinking fund transfers appear as line items in the budget. Every dollar is accounted for. This is the tightest integration.

Sinking Funds + 50/30/20 Rule

Sinking fund contributions generally live in the “Needs” or “Savings” bucket depending on whether they cover essential expenses (car insurance = Needs) or lifestyle expenses (vacation = Savings). The 20% savings portion covers both the emergency fund and sinking funds — so allocation between them matters. Read our Zero-Based Budgeting vs 50/30/20 comparison for a full breakdown of how each handles irregular expenses.

Sinking Funds + Envelope Budgeting

The physical envelope method places cash into labelled envelopes for each spending category. Sinking fund envelopes work the same way — you physically move cash into a “Car Insurance” envelope each payday. The digital equivalent uses named savings sub-accounts in your bank app. The principle is identical: money is separated, labelled, and protected from other spending.

🌍 The Expat & UAE Sinking Fund Guide

Living and working outside your home country creates a unique category of predictable large expenses that domestic budgets rarely account for. These are the most important sinking funds for expats in the UAE, Saudi Arabia, and Gulf region.

Annual Flights Home

Whether you fly once or twice a year, the cost is known in advance. Divide your annual flight budget by 12 and automate a monthly transfer. A $2,400/year flight budget means $200/month into this fund — starting January, not October.

Visa Renewal & PRO Fees

UAE residence visa renewals, Emirates ID renewals, medical fitness tests, and PRO service fees are predictable annual or bi-annual expenses. These can total AED 3,000–6,000 per renewal cycle. Monthly contribution: AED 250–500.

Gratuity (End-of-Service)

Your UAE or KSA gratuity is technically your employer’s sinking fund for you — they’re obligated to pay it when your contract ends. But many expats don’t account for the income gap between leaving one job and starting the next. Use our free UAE & KSA Gratuity Calculator to calculate your entitlement and build a personal transition fund alongside it.

Shipping & Relocation Costs

If there’s any chance your contract ends or you relocate within 2–3 years, a relocation fund of $200–$400/month is one of the highest-value funds an expat can hold.

Home Country Property Costs

Many expats own or maintain property in their home country. Maintenance, taxes, and management fees continue whether you’re there or not. A dedicated home-country property sinking fund protects both your UAE finances and your overseas asset.

Know Your Exact Sinking Fund Contribution Per Hour Worked

Convert your salary to an hourly rate and see what each sinking fund contribution really costs in working time. Free, instant, no signup.

Calculate My Hourly Rate →Sinking Fund Tracking — Apps and Tools That Help

The best tracking system for your funds is the one you’ll actually use. Here are the most effective options from fully manual to fully automated.

| Tool | Approach | Best For | Cost |

|---|---|---|---|

| YNAB (You Need A Budget) | Zero-based, every dollar assigned | Detailed budgeters who want full visibility | $14.99/month |

| Multiple bank sub-accounts | Separate named savings accounts | Simplest effective system — no extra app needed | Free |

| Google Sheets / Excel | Manual spreadsheet tracking | People who want full control and customisation | Free |

| Monzo / Starling pots | Built-in savings pots with names | UK and EU users — excellent built-in fund separation | Free |

| PocketGuard | Automated budget tracking | People who want a simple overview | Free / $34.99/yr |

| Physical cash envelopes | Manual envelope budgeting | Visual learners who prefer tangible money | Free |

For most people, the simplest system that actually works is multiple named savings accounts at an online bank. No extra app, no subscription, and the balance is visible every time you open your banking app. According to NerdWallet, most high-yield online savings accounts now offer unlimited sub-accounts with custom names at no charge.

One Response

[…] more on managing your money once you know what you’re earning, see our guides on how to set up a sinking fund, zero-based budgeting vs 50/30/20, and how to stop living paycheck to […]